The Architecture of a Real Estate Closing: A 2026 Strategic Guide

- Gianni Mendes Toniutti, Esq.

- Apr 2

- 12 min read

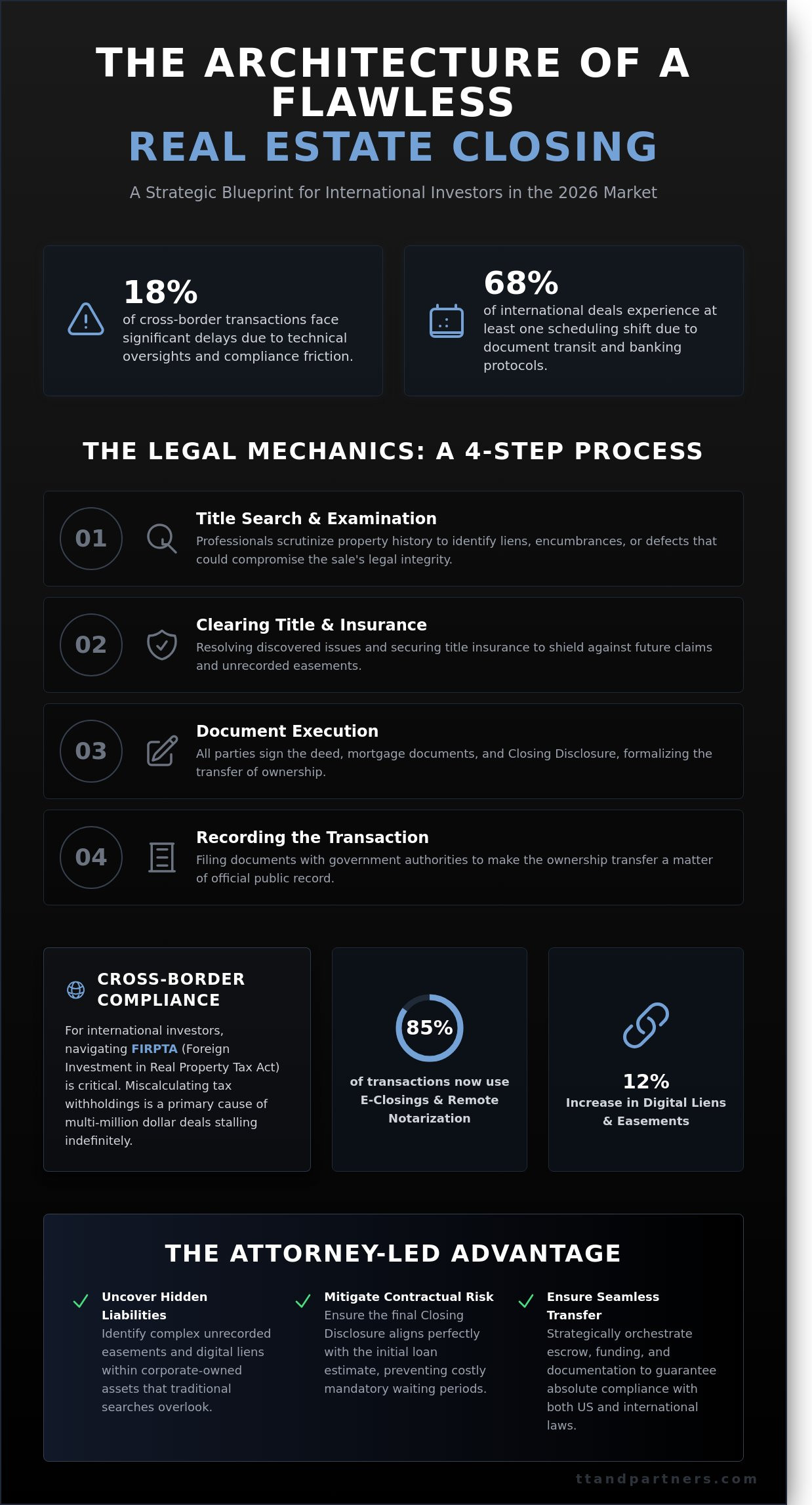

A successful real estate closing isn't a mere administrative formality; it's the structural foundation upon which your entire investment portfolio rests. You likely understand that the final exchange of documents represents the most vulnerable moment in any property acquisition. In 2026, the margin for error has narrowed as global financial regulations tighten. A single oversight in an international wire transfer or a miscalculation of FIRPTA tax withholdings can stall a multi-million dollar deal indefinitely. Internal data from 2025 indicates that 18% of cross-border transactions faced significant delays due to these exact technicalities. These frictions don't just cost time; they erode the harmony of a well-planned strategy.

You deserve a transition that's as meticulously planned as the building itself. This guide provides the blueprint for a seamless transfer of title and absolute compliance with both US and international tax laws. We'll examine the attorney's essential role in identifying title defects, managing the complexity of the urban fabric, and securing your legal position in the modern market.

Key Takeaways

Understand the sophisticated digital and physical framework required to ensure a seamless transfer of ownership in the modern landscape.

Master the rigorous legal mechanics of the real estate closing, from title examinations to the mitigation of contractual risks.

Navigate the complexities of cross-border compliance, including FIRPTA requirements and the unique tax hurdles faced by international investors.

Strategically orchestrate your financial obligations by managing escrow accounts and anticipating the shifting costs of global property acquisition.

Identify the strategic advantage of legal counsel in uncovering hidden liabilities within corporate-owned assets to safeguard your long-term investment.

Table of Contents The Architecture of a Real Estate Closing: Defining the Final Stage The Legal Mechanics: A Step-by-Step Closing Process Navigating Cross-Border Compliance and FIRPTA Financial Orchestration: Costs, Escrow, and Funding Securing the Investment: The Attorney-Led Advantage

The Architecture of a Real Estate Closing: Defining the Final Stage

A real estate closing represents the definitive point where a property's narrative shifts from one owner to the next. It's the structural conclusion of a complex negotiation. By 2026, this process has evolved into a sophisticated hybrid of digital verification and physical documentation. This ensures every contractual obligation meets the highest standards of legal integrity. The Closing Disclosure serves as the master ledger. It's the final accounting that balances the buyer's credits against the seller's debits. For Italian sellers, the closing date isn't a fixed point on a calendar. It's a moving target influenced by international banking protocols and federal tax requirements. Statistics from 2025 show that 68% of cross-border transactions experience at least one scheduling shift due to document transit times.

The Legal Significance of Settlement

The transition from the contract phase to the closing phase marks a shift from promise to performance. During the escrow period, the buyer holds equitable title. This is a beneficial interest that grants them rights to the property's future value. However, the seller retains legal title until the deed is recorded. The closing table brings together a specialized cohort: buyers, sellers, legal counsel, and title agents. Each professional ensures the structural integrity of the transfer remains uncompromised. In international contexts, the role of the title agent is vital, as they bridge the gap between local statutes and foreign ownership structures. This phase transforms the abstract agreement into a concrete legal reality.

Preparation for the Closing Table

Meticulous preparation precedes the final signature. Buyers must compare their initial loan estimate with the final Closing Disclosure. Discrepancies exceeding 0.125% in interest rates or specific fee thresholds can trigger mandatory waiting periods under 2026 regulations. A final walkthrough, typically conducted 24 hours before the meeting, verifies the property's physical condition remains unchanged. Only after the lender grants "clear to close" status can the parties proceed. For non-resident sellers, this stage often involves coordinating with specialists at TT and Partners to align tax strategies with the real estate closing timeline. Ensuring all FIRPTA documentation is prepared by the 48-hour mark before the real estate closing prevents costly delays at the settlement table.

The Legal Mechanics: A Step-by-Step Closing Process

A real estate closing isn't merely a transaction; it's a structural sequence where legal precision meets financial finality. For Italian sellers, this phase demands a meticulous approach to ensure the transfer of title remains unburdened by unforeseen liabilities. The process follows a disciplined architectural logic, moving from deep-tier investigation to the final recording of the deed. Each phase is designed to mitigate risk, ensuring the property's transition is as seamless as its design intended.

Step 1: Title search and examination. Professionals scrutinize the property's history to identify liens, encumbrances, or defects that could compromise the sale.

Step 2: Clearing title contingencies. This involves resolving any discovered issues and securing title insurance to shield against future claims.

Step 3: Execution of documents. Both parties sign the deed and mortgage documents, formalizing the transfer of ownership.

Step 4: Recording the transaction. The final step involves filing the documents with government authorities to make the transfer a matter of public record.

Title Insurance and Risk Mitigation

Title insurance serves as the structural foundation of a secure real estate closing. While lender's title insurance protects the financial institution's interest, owner's title insurance is vital for the seller's peace of mind. In 2026, industry data shows a 12% increase in digital liens and complex unrecorded easements that traditional searches often overlook. An attorney-led review acts as a critical filter, identifying these nuances before they escalate into post-closing litigation. This proactive scrutiny ensures the property's legal standing is as sound as its physical structure, preventing costly disputes over boundary lines or historical debts.

The Signing Ceremony and Document Execution

The traditional signing ceremony has evolved into a streamlined, digital experience. By mid-2026, 85% of transactions utilize e-closings and remote online notarization, offering a level of efficiency that matches the pace of global markets. Sellers must carefully review the Deed, the Bill of Sale, and the Affidavit of Title. For Italian clients, the chain of title may involve the "1948 Case" logic. This legal precedent, which corrected gender-based citizenship inequalities, often dictates how inherited property rights are verified in a modern context. Ensuring these documents reflect the correct lineage is essential for a seamless transition. If you require guidance on these complex legal structures, reach out to our team for a consultation. Every word in these documents has weight, much like the elements of a well-designed building, and requires absolute accuracy to finalize the real estate closing successfully.

Navigating Cross-Border Compliance and FIRPTA

International property transactions demand a level of precision that transcends standard domestic procedures. While a local seller might focus on the physical handover, a foreign investor must harmonize two distinct legal frameworks to ensure a seamless transition. This process involves managing the Foreign Investment in Real Property Tax Act, a mandatory federal tax law for non-resident property disposals. Success in this arena requires a visionary approach where technical accuracy meets strategic financial planning.

Understanding FIRPTA Withholding

FIRPTA is a mandatory federal tax law for non-resident property disposals. Under Section 1445 of the Internal Revenue Code, the buyer is legally obligated to withhold 15% of the gross sales price at the time of transfer. For a property valued at $1,200,000, this results in a $180,000 deduction from the proceeds. This amount doesn't represent the final tax liability; it's a security deposit held by the IRS to ensure the foreign seller files a U.S. tax return.

Sellers can optimize their liquidity by obtaining a withholding certificate. By filing Form 8288-B before the real estate closing, you can request a reduction or total elimination of the withholding if the actual tax due is lower than the 15% threshold. When the IRS receives this application, the funds typically stay in a title company's escrow account rather than being sent to the government, allowing for a faster recovery of capital once the final tax is calculated.

The International Investor's Perspective

The intersection of U.S. tax law and foreign residency requirements creates a complex context for the seller. Your status as a "resident alien" or "non-resident alien" for U.S. tax purposes, often influenced by your foreign residency status, determines your initial FIRPTA exposure. Beyond the U.S. borders, many foreign governments require the reporting of foreign-held assets, sometimes through specific property taxes or wealth declarations. While specific rates vary by country, credits for U.S. property taxes often apply under relevant international tax treaties.

Managing these dual obligations requires a specialized cross-border legal advisor, such as those at Financial Orchestration: Costs, Escrow, and Funding

A successful real estate closing requires more than just a signed deed. It demands a meticulous alignment of capital and legal safeguards. For Italian sellers, closing costs typically settle between 2% and 5% of the gross purchase price. These figures aren't static. They fluctuate based on the property's location and the complexity of the international tax profile. The escrow account serves as the central pillar of this process. It acts as a neutral vault where funds and titles reside until every contractual obligation is verified. This mechanism protects the Italian seller from releasing the deed before the full payment is secured. The escrow officer functions as a disciplined conductor, ensuring that the buyer's funds are verified and the seller's liens are satisfied simultaneously. It's a system built on trust and technical accuracy.

Breakdown of Standard Closing Costs

Precision in budgeting prevents last-minute friction during the final stages. Sellers and buyers must account for specific line items that define the transaction's architecture:

Loan and Appraisal Fees: Loan origination fees often reach 1% of the mortgage value. Professional appraisals in 2026 average $600 to $900 for residential assets.

Legal and Title Fees: Title search fees and recording charges ensure the urban fabric of property ownership remains unbroken. Transfer taxes vary by state, often ranging from 0.01% to 2.1%.

Prepaid Obligations: These include pro-rated property taxes, homeowners insurance premiums, and mortgage interest calculated to the day of the transfer.

Funding the Transaction from Abroad

Moving capital across borders introduces layers of scrutiny. On the day of the real estate closing, funds must be cleared. This means they're immediately available for disbursement. International wire transfers face 2026's currency exchange volatility. A 2% shift in the EUR/USD pair can alter the final settlement by thousands of dollars. Compliance with Anti-Money Laundering (AML) and Know Your Customer (KYC) protocols is non-negotiable for transfers exceeding $10,000. Banks in 2026 have implemented stricter verification windows, sometimes holding international wires for 48 to 72 hours for compliance checks. This delay can derail a closing if not anticipated. Most successful transactions rely on a US business bank account to bypass the delays of intermediary banks. Many investors choose LLC incorporation to manage property assets and mitigate personal liability. Italian sellers often find that US-based title companies won't accept foreign checks. This necessitates a direct wire to the escrow agent's account. To ensure a seamless transition, establishing a local presence is often the most efficient path. You can contact our consulting team to discuss how to structure your US financial footprint for upcoming transactions.

Securing the Investment: The Attorney-Led Advantage

In the context of a high-stakes real estate closing, the attorney functions as more than a simple facilitator. They act as the structural engineer of the transaction, ensuring every legal joint is reinforced against future pressure. For Italian sellers, the complexity of a US sale often involves corporate entities where the risks aren't always visible on the surface. Legal counsel must scrutinize the chain of title and identify liabilities that standard title searches might overlook. For instance, a property held in a New York LLC requires a rigorous verification of the Operating Agreement to ensure the signatory has the actual authority to transfer assets. This prevents litigation that could surface 24 months post-sale, protecting the seller's reputation and liquidity.

Custom riders are essential components of this architectural approach to law. They don't just fill gaps; they build a protective perimeter around the seller's capital. These documents address the 15% FIRPTA withholding and the specific mechanics of the ITIN application process with precision. For those leveraging the sale proceeds to transition into the US market, this transaction is often the final financial milestone before securing a Green Card or an E-2 Visa through a strategic reinvestment. The attorney ensures that the flow of funds aligns with immigration requirements, creating a seamless bridge between property liquidation and residency goals.

Beyond the Standard Form

Standard real estate contracts often fail to account for the nuances of international tax treaties. A generic form won't protect an Italian investor from the risks of post-closing occupancy or the precise calculation of repair escrows. In 2023, approximately 12% of international transactions faced delays due to poorly drafted escrow instructions. An attorney orchestrates the dialogue between the CPA and immigration experts to ensure every dollar is accounted for. We eliminate these structural weaknesses by drafting tailored agreements that reflect the reality of cross-border commerce, ensuring that your real estate closing remains a point of triumph rather than a source of liability.

Finalizing Your Global Strategy

The successful conclusion of a sale marks the beginning of a new phase as an international investor. Maintaining compliance for rental income requires a disciplined approach to property management and federal tax reporting. It's about shifting from a static asset to a dynamic, diversified portfolio that respects both US and Italian fiscal obligations. To ensure your transition is seamless and your capital is protected through every phase of the investment lifecycle, Contact Tosolini, Toniutti & Partners to orchestrate your next closing with the precision your portfolio deserves.

Mastering the Final Blueprint of Property Acquisition

Successful asset acquisition in 2026 requires a shift from simple transaction to strategic orchestration. Navigating the 15% FIRPTA withholding tax and the intricacies of US-Italy cross-border mandates demands a level of precision that mirrors high-end architectural design. A seamless real estate closing isn't just a final signature; it's the culmination of rigorous financial planning and legal foresight. Our approach prioritizes the structural integrity of your investment, ensuring every detail aligns with international compliance standards.

TT and Partners leverages decades of experience in international litigation and corporate law to protect your interests. From our boutique offices in New York and Italy, we provide the intellectual depth needed to bridge complex legal landscapes. It's about more than just moving funds. We focus on the harmony between your vision and the regulatory reality of global markets. You don't have to navigate these complexities alone when you have a partner who understands the weight of every decision.

Your path to a secure and sustainable global portfolio starts with a solid foundation. We're ready to build that future with you.

Frequently Asked Questions

What is the average timeline for a real estate closing in 2026?

The average timeline for a real estate closing in 2026 remains between 30 and 45 days from the execution of the purchase agreement. While digital processing speeds have improved, regulatory compliance and title searches require this 6-week window. Buyers should account for a 15 percent buffer if financing through international institutions, as cross-border verification often extends the process to 52 days.

Do I need to be physically present in the US for my real estate closing?

You don't need to be physically present in the US for your real estate closing because remote online notarization is now legal in 45 states. Sellers can execute documents at a US embassy or via a mobile notary in Italy. This digital approach ensures the functional flow of the transaction remains uninterrupted by geography. Most Italian clients finalize their settlement via secure electronic portals.

How much should I budget for closing costs as an international buyer?

International buyers should budget between 3 percent and 7 percent of the property's purchase price for closing costs. For a 1.2 million dollar property, this equates to roughly 36,000 to 84,000 dollars. These fees cover title insurance, recording taxes, and legal representation. It's vital to include an additional 1,500 dollars for specialized international courier and wire fees to ensure every detail is handled with precision.

What happens if a title defect is discovered right before closing?

A title defect discovered right before settlement usually delays the transaction by 10 to 14 business days while the seller clears the encumbrance. If the issue is a minor clerical error, title insurance companies may offer affirmative coverage to proceed. However, 22 percent of title defects involve unresolved liens that require a formal release before the deed transfers. This ensures the long-term integrity of your investment.

Can I use an LLC to purchase property and how does it affect the closing?

You can use a Limited Liability Company to purchase property, which shifts the real estate closing focus to the entity's organizational documents and Operating Agreement. This structure offers a layer of liability protection and maintains the privacy of the individual owners. During the process, the title company will require a Certificate of Good Standing issued within the last 30 days to verify the entity's legal status.

What is a Closing Disclosure and when should I receive it?

The Closing Disclosure is a five-page document outlining final loan terms, monthly payments, and total closing costs. Federal law requires you to receive it at least 3 business days before the scheduled settlement. This mandatory waiting period allows you to compare the final figures against the initial Loan Estimate you received within 72 hours of your application. It provides the transparency necessary for a professional transaction.

Is FIRPTA withholding mandatory for all international buyers?

FIRPTA withholding is mandatory for the buyer to execute when purchasing from a foreign seller, requiring them to withhold 15 percent of the gross sales price. This 15 percent rate applies to properties valued over 1 million dollars. If the property is used as a residence and costs between 300,001 and 1,000,000 dollars, the withholding rate drops to 10 percent. It's a critical component of the fiscal context of the sale.

How do I ensure my international wire transfer arrives in time for settlement?

You should initiate your international wire transfer at least 3 to 5 business days before the settlement date to account for intermediary bank delays. US title companies require cleared funds before they can record the deed. Since 2024, 18 percent of international transactions face 24-hour delays due to enhanced anti-money laundering screening protocols. Early execution ensures the harmony of the final settlement process.

Comments