International Inheritance Law Italy: The 2026 US-Italy Strategic Guide

- Gianni Mendes Toniutti, Esq.

- May 10

- 13 min read

What if your carefully drafted US Will is treated as a mere suggestion by Italian authorities? For many families, the assumption that testamentary freedom crosses the Atlantic ends abruptly when faced with the rigid structure of Italian forced heirship. It's natural to feel anxious about how the Italian Revenue Agency's bureaucracy might impact your legacy, especially when the threat of double taxation looms over cross-border assets. We believe that managing international inheritance law Italy is not a conflict of laws; it's a deliberate harmonization of two distinct legal architectures.

This strategic guide provides the clarity you need to master these complexities using the expert legal frameworks established for 2026. You'll gain a clear roadmap for the Italian probate process while learning how to minimize tax burdens under the latest reforms. We'll examine the separate one million Euro tax-free thresholds for gifts and inheritance effective January 1, 2026, and the shift to mandatory self-assessment. By understanding these structural shifts, you can ensure your assets pass to your chosen heirs with precision and peace of mind. At Tosolini, Toniutti & Partners, we specialize in building these legal bridges for US-based families with legacy interests in Italy.

Key Takeaways

Identify how the principle of habitual residence dictates the governing law of your estate and how to proactively utilize a choice of law clause to maintain control.

Distinguish between the Legitimate Portion reserved for family members and the Disposable Portion to understand exactly which assets you are free to bequeath.

Master the 2026 fiscal landscape of international inheritance law Italy, including the new mandatory self-assessment regime and the separate one million Euro tax-free thresholds for gifts and legacies.

Follow a precise roadmap for the Italian probate process, from obtaining a Tax Code to filing the Declaration of Succession within the mandatory twelve month window.

Discover why a strategic, architectural approach to estate planning is essential to harmonize US and Italian legal frameworks and prevent the risks of double taxation.

Table of Contents

Conflict of Laws: Harmonizing US and Italian Inheritance Frameworks

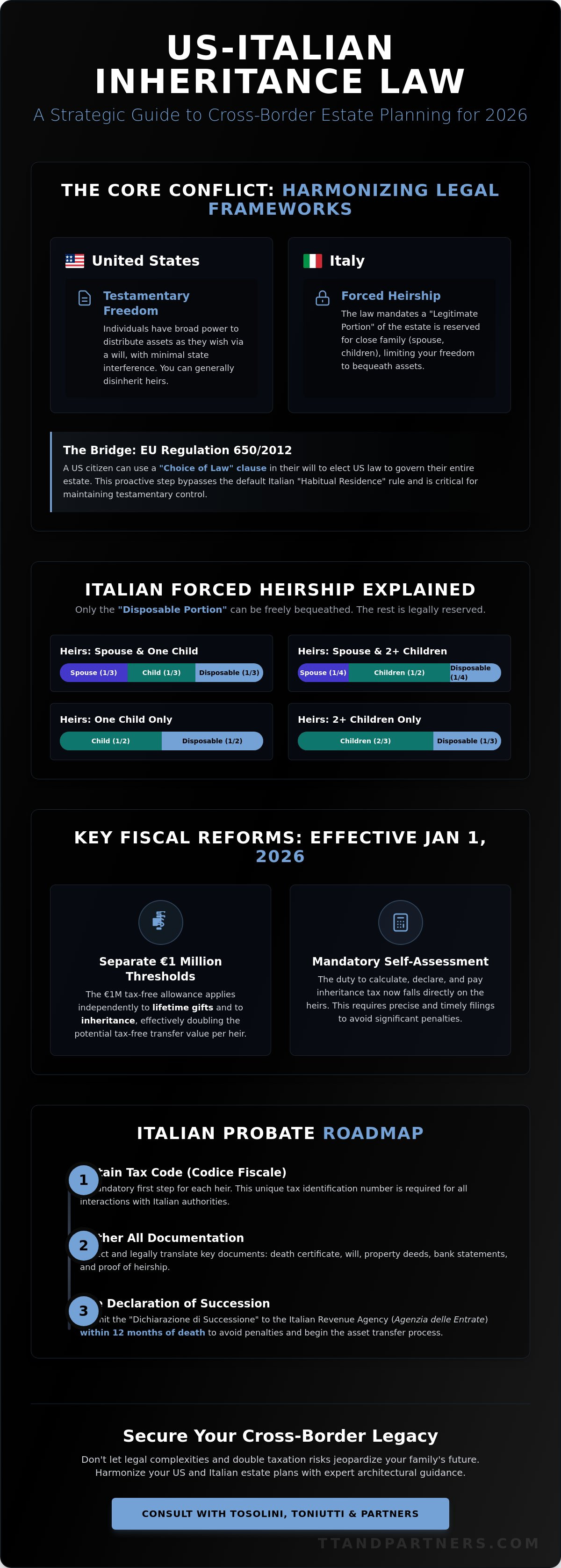

The structural integrity of an estate plan often falters at the shoreline of the Atlantic. In the United States, common law systems prioritize testamentary freedom, allowing individuals to distribute their assets with minimal state interference. Conversely, Italy’s civil law tradition operates on a rigid framework of family protection. This fundamental tension creates a complex environment for those managing international inheritance law Italy, where a US Will might be legally valid in New York but practically unenforceable in Rome. Understanding this divergence is the first step in building a resilient legacy that respects both jurisdictions.

Under current EU standards, the principle of Unity of Succession dictates that a single law should govern the entirety of a deceased person's estate regardless of asset location or type. This principle aims to prevent the fragmentation of an estate across multiple legal systems. However, the default trigger for this governing law is the deceased's last habitual residence at the time of death. If a US citizen dies while residing in Tuscany, Italian law may automatically apply to their worldwide assets, including bank accounts in Delaware or real estate in Florida. The Italian Civil Code views the estate as a holistic entity, often asserting jurisdiction over foreign situated assets unless a specific legal intervention is made.

Common Law vs. Civil Law: A Structural Divergence

US Wills face significant challenges within the Italian probate system because they often lack the formal notarial requirements essential to Italian civil law. While a US court might accept a handwritten note or a witness signed document, an Italian notary requires a specific level of authentication to transfer title. The concept of testamentary freedom in the US allows you to disinherit almost anyone; however, Italy’s forced heirship laws mandate that a specific percentage of the estate must go to reserved heirs like spouses and children. Tosolini, Toniutti & Partners bridges this gap by treating the estate plan as a technical blueprint. We ensure that US legal intent is translated into a format that satisfies Italian building codes for succession. While the Italian inheritance tax system focuses on the fiscal value of the transfer, the underlying legal right to the property must be secured first.

The Impact of EU Regulation 650/2012 on US Citizens

Strategic planning allows US citizens to bypass the default habitual residence rule through a choice of law clause. EU Regulation 650/2012 grants individuals the right to choose the law of their nationality to govern their entire succession. This is a powerful tool for maintaining international inheritance law Italy compliance while preserving US style testamentary freedom. There are limits, though. Italian public policy can occasionally override foreign intent if it is deemed fundamentally contrary to Italian social values. A professionally drafted international codicil is not just a suggestion; it is a necessity to ensure these choices are recognized by Italian authorities. To align your legacy with these dual requirements, you can coordinate with our experts at Tosolini, Toniutti & Partners for a comprehensive legal audit.

Forced Heirship and the Rights of Reserved Heirs in 2026

In the structural design of an estate, the "Quota di Legittima" acts as a foundational pillar that cannot be removed by mere intent. While US law prizes the individual's right to choose, Italian forced heirship rules establish a protected zone for close family members. This "Legitimate Portion" ensures that spouses, children, and in certain cases, ascendants, receive a fixed percentage of the deceased's assets. For those navigating international inheritance law Italy, the remaining portion is the "Quota Disponibile." This is the only segment of the estate where testamentary freedom truly applies. As of May 2026, legal interpretations have further solidified the rights of civil partners, ensuring their inclusion in this protective framework mirrors that of traditional spouses, while cohabitants now benefit from more robust protections against claims from distant relatives.

Calculating the Reserved Portions

Precision in calculation is vital for estate harmony. If a deceased leaves a spouse and one child, the estate is divided into thirds: one-third for the spouse, one-third for the child, and one-third as the disposable portion. When multiple children are involved, the spouse's share is 25%, the children collectively share 50%, and the remaining 25% is disposable. If no children exist but parents are alive, these ascendants claim a 33% share. A critical component of this calculation is the "collation" of lifetime gifts. Under the 2026 legal landscape, any significant assets gifted during the deceased's lifetime are mathematically added back into the estate to determine the true value of the reserved portions. This prevents individuals from depleting their estate through gifts to circumvent forced heirship obligations, ensuring the structural integrity of the succession remains intact.

Challenging an Italian Will from the United States

When a Will fails to respect these statutory boundaries, heirs may initiate legal action to reclaim their rightful shares. US-based heirs often find themselves in complex disputes when an Italian Will ignores their reserved rights or when foreign-situated assets are not properly accounted for in the Italian declaration. Resolving these conflicts requires a sophisticated approach to international litigation, where the focus is on reconciling foreign intent with Italian civil mandates.

The mechanism for this challenge is the Action of Reduction. It's vital to recognize that Law 182/2025, which became effective on December 18, 2025, significantly altered the remedies available. While forced heirs can still claim the value of their share, they can no longer reclaim physical property from a third party who purchased it in good faith. Their claim is now limited to a monetary demand against the original recipient of the gift. By 2026, Italy has implemented enhanced efficiency standards that favor mandatory mediation before entering the court system. This shift reduces the timeline for resolution, providing a more streamlined path for heirs to secure their legacy. If you suspect your inheritance rights have been compromised, a structural review of the estate by Tosolini, Toniutti & Partners can identify the most effective path forward.

Navigating Italian Inheritance Tax and 2026 Fiscal Reforms

The fiscal landscape of 2026 demands a new level of precision from international heirs. Unlike previous years where the Italian Revenue Agency calculated the tax bill, Legislative Decree 139/2024 has fully shifted the responsibility to the taxpayer. This mandatory self-assessment model requires heirs to calculate, declare, and pay their taxes within 90 days of filing the Dichiarazione di Successione. The filing itself must occur within 12 months of the death. Failure to adhere to these windows can lead to significant penalties, making a proactive approach to international inheritance law Italy essential for protecting the estate's value.

The current tax rates remain structured by kinship: 4% for spouses and direct descendants, 6% for siblings and relatives up to the fourth degree, and 8% for all other beneficiaries. A major victory for estate planning in 2026 is the formal abolition of "Coacervo." Previously, the value of lifetime gifts was aggregated with the final estate to exhaust tax-free thresholds. Now, these are treated as separate buckets. This structural change allows for a more generous distribution of wealth across generations without the fear of retroactive tax aggregation.

The US-Italy Tax Treaty: Avoiding Double Taxation

Harmonizing two tax systems requires more than just local compliance. While a limited US-Italy treaty exists from 1955, it doesn't offer comprehensive protection against double taxation for modern estates. US citizens residing in Italy remain subject to tax on their worldwide assets. To mitigate this, heirs must strategically claim foreign tax credits on their US returns for taxes already paid to the Italian state. It's also vital to maintain rigorous FBAR and FATCA reporting to avoid IRS scrutiny. For a deeper look at these cross-border mechanics, this guide to inheriting assets in Italy for U.S. citizens provides excellent context on the intersection of these two jurisdictions.

2026 Tax Exemptions and Thresholds

The 2026 framework offers significant relief for direct family members through a €1 million tax-free threshold per beneficiary. This threshold applies separately to gifts and inheritances, effectively doubling the potential tax-free transfer to €2 million for qualifying heirs. For siblings, this separate threshold is set at €100,000. Additionally, the tax base for real estate is often calculated using the cadastral value rather than the market price, which frequently results in a lower fiscal burden. Special exemptions also apply to family-owned businesses and heirs with recognized disabilities, ensuring the transfer of legacy doesn't compromise financial stability. If you're concerned about optimizing these thresholds, you can consult with our team at TT and Partners for a tailored fiscal strategy.

The Probate Process: A Roadmap for International Heirs

The probate process in Italy functions more like an architectural restoration than a legal battle. It requires a disciplined sequence of administrative alignments to ensure the transition of assets is both permanent and legally sound. Managing international inheritance law Italy isn't just about reading a Will; it's about navigating a bureaucratic landscape that lacks the centralized court supervision common in the United States. Heirs must first verify the existence of an Italian Will through the National Registry of Wills to determine if the deceased left specific instructions regarding their Italian holdings. If no Will is found, the estate follows the statutory rules of intestate succession.

A critical administrative hurdle is the acquisition of an Italian Tax Code (Codice Fiscale) for all US-based beneficiaries. Without this identifier, no legal or fiscal transaction can proceed. Once identified, heirs must file the Declaration of Succession within the mandatory 12-month window from the date of death. It's vital to remember that filing this document is a fiscal obligation and doesn't constitute a formal acceptance of the inheritance. Acceptance can be express, through a formal notarial deed, or tacit, occurring when an heir performs an act that implies ownership. Finally, the process concludes with the Voltura Catastale, which updates the Land Registry to reflect the new ownership structure.

Real Estate Closings and Title Regularization

Discrepancies in the Italian Land Registry are common, especially with older properties that haven't changed hands in decades. Before an inherited property can be sold or even fully secured, these technical inconsistencies must be resolved. Heirs often require specialized real estate closing expertise to harmonize the physical state of the building with the official records. For heirs residing in the US, this entire process is typically managed through a Procura (Power of Attorney), allowing a representative in Italy to sign deeds and filings on their behalf without the need for international travel.

Accessing Italian Bank Accounts and Financial Assets

Italian financial institutions are notoriously conservative when dealing with foreign claimants. Banks will typically freeze accounts upon notification of death and won't release funds until they receive a certified copy of the filed Declaration of Succession and, frequently, a Notarial Act of Notoriety. This document, prepared by an Italian Notary, confirms the identity and rights of the heirs. Dealing with the Poste Italiane or private insurance policies adds another layer of complexity, as each entity has its own verification protocols. If you're struggling to secure financial assets from abroad, you can contact our legal team for direct administrative support.

Strategic Cross-Border Planning: The TT&P Partnership

A "one-size-fits-all" estate plan is a blueprint for failure when assets span two continents. In our practice, we view the management of international inheritance law Italy as an architectural challenge where every legal instrument must serve a specific functional purpose. US families often rely on domestic revocable trusts that, while efficient in New York or California, may be viewed with skepticism or mischaracterized by Italian fiscal authorities. We believe in building a resilient legal structure that accounts for the historical context of Italian property while embracing the modern financial tools of the US market. Integrating Italian citizenship goals into this process often provides a strategic advantage; it clarifies the governing law under EU 650/2012 and simplifies the administrative burden for heirs who wish to maintain a permanent connection to their heritage.

The "partnership" at the core of our name reflects our belief in a continuous dialogue between the client, their US advisors, and Italian legal frameworks. We don't see an estate as a collection of static objects. Instead, we view it as a space that must be habitable for the next generation. This requires a shift from reactive document filing to proactive structural design. By harmonizing these two legal systems, we eliminate the friction that typically leads to delays in the Italian probate process or the unnecessary erosion of wealth through inefficient tax reporting.

Designing Your International Will

Designing an international legacy requires coordinating US and Italian Wills to prevent conflicting instructions. In 2026, the Italian legal landscape has evolved to explicitly address the treatment of trusts. Effective January 1, 2026, succession tax is triggered either when assets are contributed to a trust or when they're distributed to beneficiaries. This clarity allows for more sophisticated planning, but it also means that poorly structured US trusts can inadvertently lead to higher tax exposure. We focus on proactive strategies that align the disposable portion of your estate with your US testamentary goals, ensuring the transition is seamless and the risk of family disputes is minimized through precise drafting.

The Value of Expert US-Italy Legal Counsel

Our partnership provides a bridge for US-based families, leveraging expertise in both New York legal standards and the intricacies of the Italian civil code. Beyond the immediate needs of probate, we often recommend LLC incorporation as a vehicle for managing family assets, providing a layer of protection and professional governance for inherited real estate. This holistic approach ensures that your legacy remains functional and sustainable for decades to come. If you're ready to secure your cross-border interests with the precision they deserve, contact TT and Partners for a strategic consultation that respects your family's past while planning for its future.

Securing Your Legacy Across Borders

The transition of an estate between the United States and Italy is a complex architectural feat that requires more than just standard documentation. By aligning the principles of testamentary freedom with the rigid requirements of forced heirship, you ensure that your legacy remains structurally sound. We've explored how the 2026 fiscal reforms and the shift to mandatory self-assessment place a higher premium on precision and timely action. Navigating international inheritance law Italy effectively means bridging the gap between two distinct legal cultures to protect your family's future.

At TT and Partners, we bring decades of US-Italy cross-border legal experience to every consultation. With a strategic presence in both New York and Italy, our team possesses the rare expertise required to operate within both Common Law and Civil Law systems. We don't just file papers; we design resilient legal frameworks tailored to your unique context. Secure your cross-border legacy—Contact TT&P for an inheritance consultation. It's time to transform your global assets into a lasting and harmonious heritage.

Frequently Asked Questions

Does an Italian Will override my US Will for property in Italy?

An Italian Will does not inherently override a US Will; however, they must be harmonized to prevent conflicting instructions. While Italian authorities recognize valid foreign Wills under EU standards, having a specific Italian Will for local assets ensures a smoother probate process. This prevents the administrative delays and costs associated with translating and validating a US probate court's decree before an Italian notary.

What happens if an Italian relative dies without a Will (Intestacy)?

If a relative dies intestate, the estate is distributed according to the strict hierarchy defined in the Italian Civil Code. The spouse and children receive the primary shares. If a deceased leaves a spouse and two children, the spouse receives 33% and the children share the remaining 66%. This process is entirely administrative and leaves no room for the flexibility found in planned successions.

How much is the inheritance tax in Italy for US citizens in 2026?

As of May 2026, the tax rates are 4% for spouses and direct descendants, 6% for siblings and relatives up to the fourth degree, and 8% for all other heirs. Spouses and children benefit from a €1 million tax-free threshold per beneficiary. This threshold is now separate for gifts and inheritances, allowing for a more efficient transfer of wealth under the current international inheritance law Italy framework.

Can I renounce an Italian inheritance if it includes significant debt?

You can renounce an inheritance if the liabilities exceed the value of the assets. This declaration must be made formally before an Italian Notary or through an Italian consulate. Another option is accepting "with benefit of inventory," which limits your liability for the deceased's debts to the value of the inherited assets, protecting your personal US-based wealth from Italian creditors.

Do I need to travel to Italy to claim my inheritance?

Travel is not required to manage the probate process. Most US heirs utilize a Procura Speciale, a specific Power of Attorney that allows a legal representative in Italy to act on their behalf. This representative can obtain your Codice Fiscale, file the Declaration of Succession, and manage bank account releases, ensuring the process moves forward without the need for international travel.

What is the deadline for filing an Italian inheritance tax return?

The Dichiarazione di Successione must be filed within 12 months of the date of death. Following the 2025 fiscal reforms, heirs are also responsible for a mandatory self-assessment. This means you must calculate and pay the inheritance tax within 90 days of filing the declaration. Missing these windows can result in penalties reaching 120% of the tax due, plus interest.

How does EU Regulation 650/2012 affect my US estate plan?

EU Regulation 650/2012 allows you to choose the law of your nationality to govern your entire estate, including assets in Italy. By including a specific Choice of Law clause in your Will, you can bypass Italian forced heirship rules in favor of US testamentary freedom. Without this clause, Italian law may automatically apply if Italy is considered your last habitual residence at the time of death.

Can I sell inherited Italian property immediately after probate?

You can sell the property once the Declaration of Succession is filed and the Land Registry is updated through the Voltura Catastale. In 2026, all property sales also require a certificate of "urbanistic compliance," confirming that the building's physical state matches the official municipal floor plans. Resolving any discrepancies early is essential for a successful real estate closing and the timely transfer of title.

Comments