Legal Requirements for Italian Citizens Starting a US LLC: 2026 Guide

- Gianni Mendes Toniutti, Esq.

- 3 days ago

- 12 min read

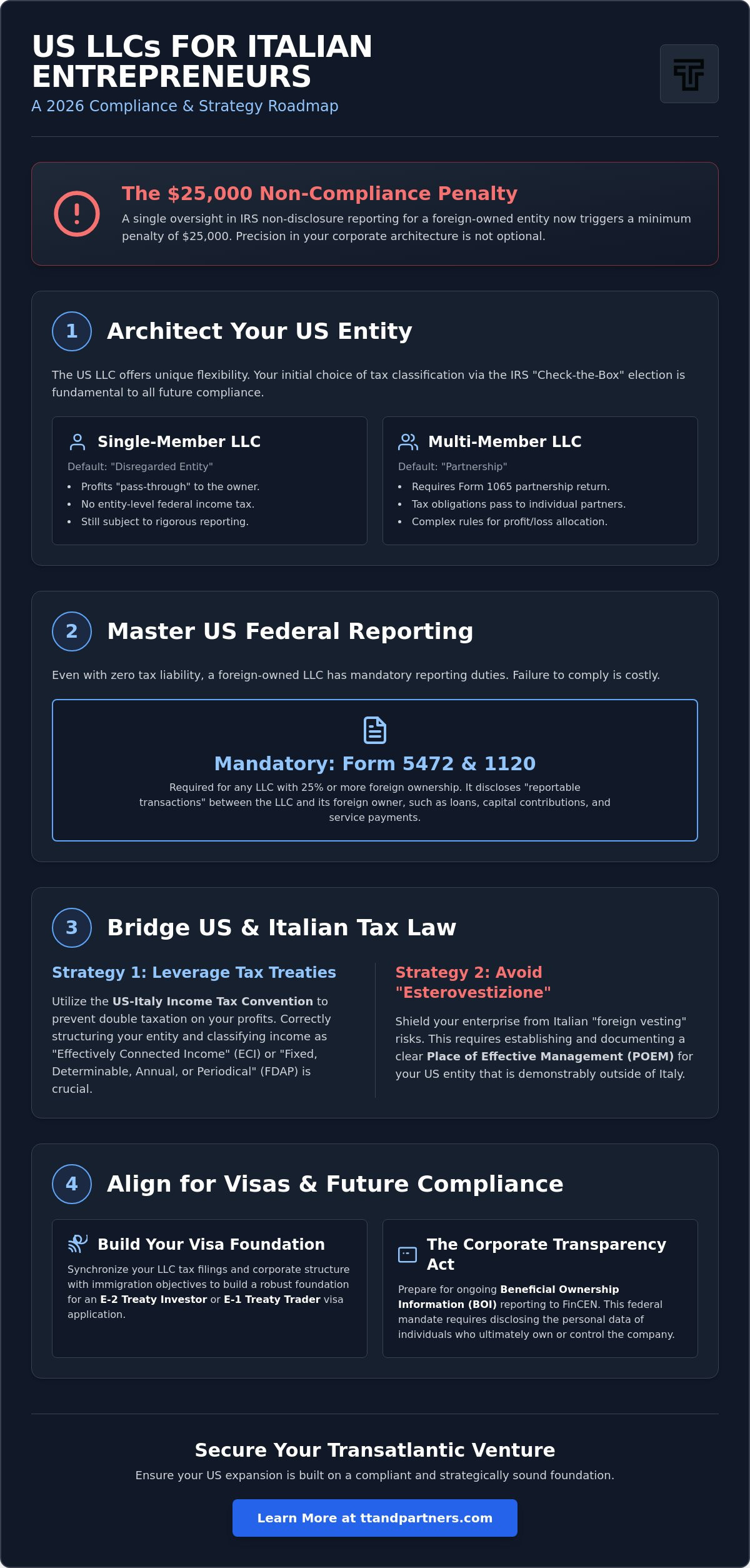

Did you know that a single oversight in IRS non-disclosure reporting can now trigger a minimum $25,000 penalty for a foreign-owned entity? For the visionary entrepreneur looking west, the legal requirements for Italian citizens starting a US LLC represent a sophisticated bridge between two distinct regulatory worlds. It's not just about simple incorporation; it's about architectural precision in your corporate structure. We understand that the fear of Italian esterovestizione laws and the hurdle of obtaining an EIN without a US Social Security Number can feel like significant barriers to your international expansion.

This 2026 guide promises to help you master the legal and tax framework of US-Italy cross-border business to ensure full compliance and optimize your investment. You'll learn how to avoid the 26% Italian dividend tax trap while positioning your enterprise for E-2 Treaty Investor visa eligibility. We'll examine the specific reporting mandates for 2026 and provide a clear roadmap to a compliant, high-performing US corporate presence that respects both American transparency and Italian fiscal obligations.

Table of Contents

The US LLC Architecture for Italian Nationals

The foundation of any successful transatlantic venture begins with the structural choice of the entity. The US LLC Architecture represents a sophisticated hybrid; it merges the robust liability protections of a corporation with the fiscal agility of a partnership. For the Italian entrepreneur, this flexibility is both a strategic advantage and a source of potential complexity. Understanding the legal requirements for Italian citizens starting a US LLC requires moving beyond simple registration. You must grasp how the IRS "Check-the-Box" regulations allow you to dictate the entity's tax classification, a process that fundamentally alters your reporting obligations from day one.

American corporate law prioritizes contractual freedom, allowing the Operating Agreement to serve as the ultimate authority on how the business is governed. This stands in stark contrast to the more rigid frameworks of the Italian Società a Responsabilità Limitata (SRL). While the US system offers immense adaptability, this fluidity must be reconciled with Italian civil and tax codes. The IRS doesn't view your LLC as a static object; it sees a dynamic structure that can be classified as a corporation, a partnership, or a disregarded entity depending on your specific elections and ownership count.

Disregarded Entities vs. Multi-Member Partnerships

By default, the IRS classifies a single-member LLC owned by a non-resident as a "disregarded entity." This means the entity itself doesn't pay federal income tax; instead, the financial activity flows directly to you as the owner. However, if you invite a partner or co-investor, the structure shifts into a partnership for tax purposes. This transition triggers the requirement for Form 1065. It's vital to recognize that any foreign ownership exceeding 25% mandates strict disclosure via Form 5472. Failing to meet these standards can result in penalties starting at $25,000 per year, making the legal requirements for Italian citizens starting a US LLC a matter of high-stakes precision.

The Pass-Through Concept in a Global Context

A common misconception suggests that US LLCs are inherently "tax-free" for foreigners. In reality, the pass-through nature simply shifts the tax burden from the entity level to the individual owner. Within a global framework, the 1999 US-Italy Income Tax Convention plays a decisive role in determining where and how your profits are taxed. Your initial selection must account for these treaty provisions to avoid the trap of double taxation. For a deeper analysis of how these structures interact with broader investment goals, consult our guide on LLC Incorporation: A Strategic Guide to US Business Architecture. This strategic alignment ensures your US presence remains a vehicle for growth rather than a source of regulatory friction.

US Federal Reporting: The Form 5472 and 1120 Trap

The administrative landscape for a US entity is often more demanding than its initial formation suggests. For an Italian national, the legal requirements for Italian citizens starting a US LLC involve a rigorous disclosure regime designed to ensure absolute transparency for foreign-owned entities. Even if your LLC is a single-member disregarded entity that pays no federal tax, it remains subject to the Form 5472 mandate if foreign ownership reaches or exceeds the 25% threshold. This form tracks "reportable transactions" between the LLC and its Italian owner. These transactions include capital contributions, loans, or even the payment of small business expenses on behalf of the entity. Failing to file this or submitting an incomplete Form 1120 Pro Forma triggers a minimum $25,000 penalty per year. This isn't a mere suggestion; it's a strict federal requirement that the IRS enforces with increasing scrutiny in 2026.

2026 Compliance: BOI and the Corporate Transparency Act

Transparency standards have evolved significantly with the Corporate Transparency Act. While an interim rule in early 2025 provided relief for certain domestic entities, the landscape remains fluid as of June 2026. Italian investors must carefully evaluate their reporting status with FinCEN to ensure they aren't inadvertently non-compliant. These regulations aim to identify the specific individuals who ultimately own or control the company. For the privacy-conscious entrepreneur, this means disclosing sensitive personal data to a secure federal database. The deadlines are strict. Newly formed 2026 entities often have shorter windows to report their Beneficial Ownership Information (BOI) compared to older structures. Precision matters. If you're unsure about your specific reporting obligations, it's wise to consult with a professional strategist who understands the intersection of US and Italian law.

Obtaining an EIN and ITIN as an Italian Citizen

Financial operations in the United States are impossible without the correct identification numbers. An Employer Identification Number (EIN) is your company's primary identifier for banking and tax purposes. Since Italian residents don't have a US Social Security Number, they must apply via Form SS-4 through mail or fax. This manual process often takes several weeks and requires absolute accuracy to avoid rejection. Simultaneously, an Individual Taxpayer Identification Number (ITIN) may be necessary for personal tax filings or claiming benefits under the US-Italy tax treaty. These numbers are the keys to unlocking US business banking platforms like Mercury or Relay. They're also foundational for E-2 and E-1 Visa Success. Establishing these credentials correctly from the start prevents future delays in your commercial expansion.

US-Italy Tax Treaty: Mitigating Double Taxation in 2026

The 1999 US-Italy Income Tax Convention serves as the primary instrument for balancing fiscal obligations across the Atlantic. It's the cornerstone of any sophisticated cross-border strategy. For the Italian entrepreneur, the primary challenge lies in defining the Permanent Establishment (PE) threshold under Article 5. If your US LLC maintains a fixed place of business or exercises the authority to conclude contracts in the United States, you've likely created a PE. This status subjects your Effectively Connected Income (ECI) to US federal taxation. Understanding the legal requirements for Italian citizens starting a US LLC involves a meticulous analysis of these treaty provisions to determine if your activities trigger US tax liability or remain taxable only in Italy.

Claiming treaty benefits is essential for optimizing cash flow. Without the treaty, the IRS typically imposes a flat 30% withholding tax on Fixed, Determinable, Annual, Periodical (FDAP) income, such as dividends and royalties. However, the convention reduces these rates significantly. Dividends may be taxed at just 5% for direct ownership or 15% for other distributions. Interest often sees a 10% rate, while certain royalties can drop to as low as 0%. These reductions aren't automatic. They require the submission of Form W-8BEN or W-8BEN-E, ensuring the IRS recognizes your status as a resident of a treaty partner country.

US Federal Rates vs. Italian IRPEF/IRES

The fiscal disparity between the two nations requires careful architectural planning. While the US federal corporate tax rate is currently 21%, Italian residents often face a more complex landscape. If the LLC is treated as a pass-through, the income is subject to Italian IRPEF graduated brackets. Alternatively, a 2024 elective regime allows an Italian parent company to pay a 15% substitute tax on the LLC's profits to satisfy Controlled Foreign Company (CFC) rules. This is a strategic alternative to the standard 26% substitute tax often applied to distributions from "opaque" foreign entities. Aligning these rates ensures your US "draw" doesn't become a double-taxed liability.

Foreign Tax Credits (FTC) and Timing

Avoiding double taxation relies heavily on the Foreign Tax Credit (FTC) mechanism. Taxes paid to the IRS on ECI can generally be used as a credit against your Italian tax liability, but the timing is often a source of friction. The US and Italian tax years and filing deadlines don't perfectly align. This can lead to temporary liquidity issues if a credit isn't recognized in the same fiscal period the tax was paid. If treaty interpretations lead to conflict, our guide on International Litigation 2026: A Strategic Guide to US-Italy Legal Disputes provides a framework for managing high-stakes disagreements. Always verify that your IRS Form 5472 Filing Requirements are fully satisfied; the IRS may deny treaty benefits to entities that fail their mandatory disclosure obligations.

Strategic Compliance: Reconciling US Pass-Throughs with Italian Opacity

A fundamental friction exists between the American view of an LLC as a transparent pass-through and the Italian interpretation of foreign entities as opaque corporate structures. While you may have satisfied the legal requirements for Italian citizens starting a US LLC in Delaware or Wyoming, the Agenzia delle Entrate often maintains a different perspective. The primary risk is "esterovestizione," or tax inversion. If the Italian authorities determine that the Place of Effective Management (PoEM) resides within Italy, they'll claim the right to tax the LLC as a domestic resident company. This reclassification can lead to aggressive back-tax assessments and significant penalties, regardless of your US compliance status.

To defend against these allegations, you must establish genuine economic substance within the United States. This goes beyond a mere registered office. Maintaining a US business bank account, utilizing a local mailing address, and ensuring that strategic decisions are documented with a clear nexus to US operations are critical steps. Substance is the only shield against the presumption that the entity exists solely to circumvent Italian fiscal obligations. If your US structure lacks these hallmarks, it remains vulnerable to being treated as a "fictitious" foreign company by Italian auditors. Strategic alignment with the 15% elective substitute tax regime introduced in 2024 can also help satisfy Controlled Foreign Company (CFC) rules by providing a compliant path for reporting LLC profits in Italy.

Preferential Italian Regimes for 2026

Certain Italian tax incentives can harmonize with a US expansion. For high-net-worth individuals, the Article 24-bis flat tax of €200,000 provides a predictable cap on foreign-sourced income, simplifying the treatment of US LLC distributions. Similarly, the 7% pensioner regime in Southern Italy offers a favorable path for retirees managing US-based investments. However, combining the "Forfettario" regime with a US LLC is fraught with difficulty; Italian law generally prohibits individuals from using this simplified tax bracket if they also control a foreign entity that performs similar activities. Each of these paths requires a bespoke analysis to ensure your US presence doesn't invalidate your Italian tax benefits.

Operational Best Practices for Cross-Border Owners

Success requires a strict separation of identities. You must never treat your LLC as a personal checking account; doing so invites the IRS to "pierce the corporate veil" and treat the entity as your alter ego. Documentation is your strongest defense. Keep detailed minutes of management decisions and ensure all contracts are executed in the name of the LLC. This level of professional rigor requires constant coordination between your US legal counsel and your Italian commercialista. To build a structure that withstands both US and Italian scrutiny, contact our international strategy team for a comprehensive compliance review.

Integrating Tax Strategy with E-2 and E-1 Visa Success

For the ambitious Italian entrepreneur, the legal requirements for Italian citizens starting a US LLC are rarely an end in themselves; they're the foundational layer for physical expansion. Your corporate structure serves as the primary evidence for E-2 Treaty Investor or E-1 Treaty Trader visa applications. The US Embassy in Rome scrutinizes tax filings to verify that an investment isn't "marginal." This means your LLC must demonstrate the capacity to generate significantly more income than is required to provide a minimal living for you and your family. In 2026, consistent profitability and tax contributions are the most persuasive indicators of a business's economic contribution to the United States.

Proving a "substantial investment" requires meticulous accounting of startup costs. Every dollar spent on equipment, inventory, or professional services should be documented and reflected in your LLC's initial tax returns. These filings provide an official IRS-stamped record that your capital is "at risk" and committed to the enterprise. While there's no fixed minimum dollar amount, successful E-2 applications typically showcase investments ranging from $80,000 to $300,000. For those pursuing the E-1 Treaty Trader visa, the focus shifts to the volume of trade. At least 50% of your LLC's international trade must be between the US and Italy, a metric that's verified through your entity's commercial invoices and financial statements.

Choosing the Right Entity for Your Visa Goals

The choice between an LLC and a C-Corp can influence your long-term residency prospects. While the LLC offers pass-through flexibility, a C-Corp structure is often preferred by those envisioning a future transition to a Green Card, particularly through the EB-1C category for multinational managers. Your IRS classification impacts your visa renewal prospects in 2026, as the government seeks proof of a growing, compliant entity. For a deeper look at these requirements, see our E-2 Visa Guide 2026: The Strategic Framework for Treaty Investors. This alignment ensures your legal requirements for Italian citizens starting a US LLC support both your fiscal and immigration objectives.

The Value of Dual-Perspective Legal Counsel

Navigating this intersection requires more than just a standard incorporation service. Italian investors need attorneys who possess a deep understanding of both the American and Italian legal systems. Bridging the gap between US federal compliance and Italian residency is a delicate task that demands professional precision. To ensure your structure is optimized for both tax efficiency and visa success, contact Tosolini, Toniutti & Partners for a strategic consultation. Our team provides the holistic vision necessary to transform your US business into a sustainable, compliant gateway for your international lifestyle.

Architecting Your Strategic Bridge to the US Market

Building a successful presence in the United States requires more than a simple registration; it demands a deep understanding of how two distinct legal systems interact. We've explored how meticulous federal reporting and establishing genuine economic substance are vital to protecting your venture from both IRS penalties and Italian tax reclassification. By aligning your corporate structure with the specific demands of the E-2 or E-1 visa, you transform a compliance obligation into a powerful vehicle for international growth. Mastering the legal requirements for Italian citizens starting a US LLC is truly the first step toward securing your global legacy.

Precision in these matters isn't optional. At Tosolini, Toniutti & Partners, we've dedicated our practice to bridging the legal gap between the US and Italy since our founding. Our team specializes in E-1 and E-2 visas, cross-border corporate law, and the complex intersection of US federal compliance and Italian fiscal residency. If you're ready to ensure your international investment is both compliant and optimized for success, schedule a consultation with our US-Italy cross-border legal experts today. Your vision for a transatlantic enterprise deserves a foundation built on professional excellence and strategic foresight. We look forward to helping you build it.

Frequently Asked Questions

Does an Italian-owned US LLC need to file a US tax return if it has no US income?

Yes, you must still file informational returns even if the entity has zero US-sourced income. Disregarded entities with at least 25% foreign ownership are required to submit Form 5472 and a pro-forma Form 1120 annually to the IRS. These filings are purely for transparency and track transactions between the LLC and its Italian owner, such as initial capital contributions or administrative payments.

What is Form 5472, and why is it critical for Italian LLC owners?

Form 5472 is a mandatory disclosure document for US entities that are at least 25% foreign-owned. It's critical because it tracks "reportable transactions" like capital injections, loans, or expense reimbursements. Failing to file this form results in a minimum $25,000 penalty, making it one of the most vital legal requirements for Italian citizens starting a US LLC in 2026.

How is a US LLC taxed in Italy for a resident of Italy?

Italy generally taxes US LLC profits as personal income for the resident owner under IRPEF brackets if the entity is treated as a pass-through. However, under 2024 elective regimes, an Italian parent company may pay a 15% substitute tax to satisfy Controlled Foreign Company rules. This prevents the LLC from being taxed at standard Italian corporate rates while ensuring full compliance with the Agenzia delle Entrate.

Can I use the US-Italy Tax Treaty to avoid double taxation on my LLC profits?

You can use the 1999 US-Italy Income Tax Convention to significantly reduce withholding taxes on dividends, interest, and royalties. It also allows you to claim a Foreign Tax Credit in Italy for taxes paid to the IRS on income effectively connected to a US trade or business. This mechanism is essential for ensuring that the same profit isn't depleted by dual tax claims.

What are the penalties for failing to report a foreign-owned US LLC?

The IRS imposes a minimum penalty of $25,000 per year for failing to file Form 5472 or for submitting incomplete information. If the failure continues for more than 90 days after notification, additional $25,000 penalties apply every 30-day period. These harsh financial consequences underscore the importance of maintaining rigorous federal compliance from the very first day of your US incorporation.

Do I need a US bank account for my Italian-owned LLC to be compliant?

While not a strict legal requirement for formation, a US bank account is essential for demonstrating the "economic substance" of your entity. It helps separate personal assets from business funds, which protects you from "alter ego" claims that could pierce the corporate veil. Most Italian owners use modern platforms like Mercury or Relay to manage their US financial operations remotely and securely.

How does the Corporate Transparency Act affect Italian investors in 2026?

The Corporate Transparency Act requires many entities to report Beneficial Ownership Information (BOI) to FinCEN to combat financial crimes. As of June 2026, Italian investors must remain vigilant regarding the latest filing rules for foreign-owned domestic LLCs. These regulations prioritize absolute transparency by identifying the specific individuals who ultimately exercise control or hold significant ownership over the US corporate structure.

Is it better for an Italian national to form an LLC or a C-Corp for tax purposes?

An LLC is often preferred for its pass-through flexibility, but a C-Corp may be superior if you intend to seek venture capital or transition to certain Green Card categories. The legal requirements for Italian citizens starting a US LLC vary significantly from those of a corporation. A C-Corp faces tax at the entity level, whereas a single-member LLC avoids US federal income tax by default.

Comments