Understanding US Real Estate Contracts for Foreigners: A Strategic 2026 Guide

- Gianni Mendes Toniutti, Esq.

- Jun 10

- 12 min read

A U.S. real estate contract is far more than a simple transaction record; it's a foundational pillar of your global investment architecture that must be engineered to withstand rigorous tax and immigration scrutiny. While many investors focus solely on the property's aesthetic or location, the real value lies in the structural integrity of the legal agreement. Understanding US real estate contracts for foreigners requires a shift from viewing the document as a standard formality to seeing it as a strategic tool for asset protection. It's natural to feel a sense of trepidation when faced with unfamiliar contingencies or the specialized terminology of American property law.

You're likely concerned about hidden legal traps or the sudden impact of FIRPTA withholding on your liquidity. This guide will help you master these complexities, ensuring your purchase agreement aligns perfectly with your E-2 or O-1 visa objectives. We'll explore the 2026 reporting requirements under the Corporate Transparency Act, analyze the latest shifts in realtor commission structures, and provide a framework for navigating state-level ownership restrictions. By the end, you'll have the clarity needed to transform a complex legal obligation into a secure, vision-aligned asset.

Key Takeaways

Differentiate between standardized state forms and bespoke attorney-drafted agreements to ensure your cross-border investment is protected from the outset.

Master the use of critical contingencies as a strategic exit mechanism, protecting your earnest money from unforeseen legal or financial hurdles.

Explore the structural benefits of LLC incorporation to shield personal assets and create a robust framework for long-term property management.

Navigate the technical milestones from the initial purchase agreement to the final closing statement, a vital step in understanding US real estate contracts for foreigners.

Align your property acquisition with E-2 or O-1 visa goals by integrating real estate assets into a comprehensive immigration and investment strategy.

Table of Contents

The Anatomy of a US Real Estate Purchase Agreement

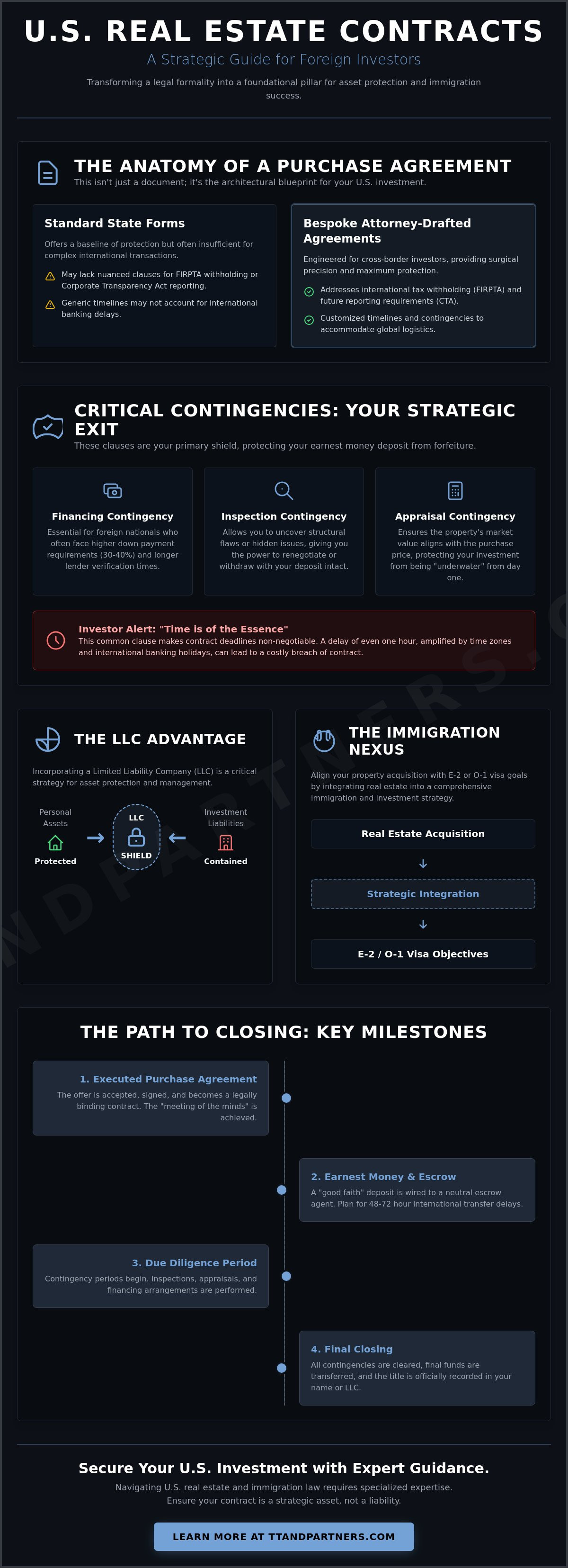

The Purchase and Sale Agreement (PSA) serves as the architectural blueprint for your U.S. investment. It’s a binding legal instrument that dictates every variable of the transaction, from the final purchase price to the specific conditions under which you can withdraw. For a non-resident, understanding US real estate contracts for foreigners begins with recognizing that these are not mere letters of intent; they are enforceable obligations that require surgical precision. The document must define the essential elements of a real estate contract, including a clear offer, acceptance, and consideration. Consideration represents the value exchanged between parties, typically the buyer's capital in exchange for the seller's equitable title.

While many residential transactions utilize standardized state forms, sophisticated investors or those in "attorney states" often require customized agreements. Standard forms offer a baseline of protection, but they may lack the nuanced clauses needed to address international tax withholding under FIRPTA or 2026 reporting requirements under the Corporate Transparency Act. The parties involved extend beyond just the buyer and seller. You'll interact with an escrow agent, who acts as a neutral stakeholder, and often specialized attorneys who ensure the structural integrity of the deal. In states like New York or Florida, the role of these professionals is distinct, and their involvement can be the difference between a secure asset and a legal liability.

The Offer vs. The Executed Contract

An offer remains a unilateral proposal until it’s signed by all parties and delivered back to the offeror. Once executed, the contract becomes the law of the transaction. U.S. law relies heavily on the "Meeting of the Minds," where both parties share a mutual understanding of every term. Foreign buyers must pay close attention to "Time is of the Essence" clauses. These provisions make deadlines for inspections or financing non-negotiable. Missing a date by even an hour can result in a technical breach, a risk significantly amplified by international time zone differences and banking holidays.

Earnest Money Deposits and Escrow

Securing a property requires a "Good Faith" or earnest money deposit, typically held in a neutral escrow account. This capital demonstrates your commitment to the seller while remaining protected by the contract's contingencies. For international investors, the primary pitfall lies in the logistics of global finance. Wire transfers from foreign banks can face 48 to 72 hour delays due to heightened anti-money laundering protocols or intermediary bank reviews. If you're coordinating a real estate closing from abroad, initiating these transfers well in advance is vital to prevent a default. Clear communication with your escrow agent ensures that your capital is positioned correctly before the contract's strict deadlines expire.

Critical Contingencies: Risk Mitigation for International Buyers

A contingency is the primary shield protecting your earnest money deposit from forfeiture. In the context of understanding US real estate contracts for foreigners, these clauses act as suspensive conditions; the contract only proceeds if specific requirements are met. For a non-resident investor, a generic contingency isn't enough. You need specific language that accounts for the logistical friction of cross-border transactions. This includes longer due diligence periods to accommodate international travel or the time required to review the new March 2026 residential reporting rules for non-financed transfers to entities.

Structuring an "exit" without penalty requires a deep understanding of the contract timeline. If an inspection reveals structural flaws, or if financing falls through, a well-drafted contingency allows you to walk away with your deposit intact. Negotiating these terms requires a balance between being a competitive buyer and maintaining a secure investment posture. It's about ensuring that your capital isn't held hostage by rigid timelines that don't account for the complexities of being an international investor.

Financing and Appraisal Contingencies

Mortgages for foreign nationals typically require a 30% to 40% down payment, a significant capital commitment that necessitates a robust financing contingency. Lenders often take longer to verify international income and assets, meaning a standard 30 day window is often insufficient. You should advocate for a 45 to 60 day financing period to avoid a technical default. While 44% of foreign buyers opted for all-cash transactions in 2025 to increase their leverage, those utilizing debt must ensure the appraisal contingency remains. This protects you if the property's valuation falls short of the purchase price, a common occurrence in volatile, high-demand U.S. markets.

Inspection and Title Contingencies

The "As-Is" contract is a frequent trap for the unwary. Even in an as-is deal, you must retain the right to inspect and terminate if the property’s condition doesn't meet your standards. Title insurance is equally non-negotiable. It protects against liens or encumbrances that could cloud your ownership. When considering your ownership structure, reviewing the IRS guidelines on LLCs provides clarity on how foreign entities can hold title while maintaining flexibility. If you're unsure how to phrase these protections, a professional real estate closing consultation can help align your contract with your long-term goals.

Strategic Ownership: LLC Incorporation for Property Acquisition

Strategic asset acquisition requires more than just a signature on a deed; it demands a robust legal shell to protect the investor's global interests. When understanding US real estate contracts for foreigners, the choice of the purchasing entity is often as critical as the price itself. Utilizing LLC incorporation allows you to separate personal liabilities from property related risks, ensuring that a localized legal dispute doesn't compromise your international holdings. While the 2026 landscape includes new transparency rules, an LLC still offers a sophisticated layer of governance that individual ownership lacks.

Privacy remains a priority for high profile investors, though it's vital to recognize the current regulatory environment. As of 2026, foreign entities registered to do business in the U.S. must report beneficial ownership information to FinCEN. Despite these reporting mandates, an LLC prevents your personal name from appearing on public land records, which provides a necessary level of anonymity from casual inquiries and predatory litigation. This structure doesn't just protect your identity; it organizes your investment into a professional business architecture that's easier to manage across borders.

LLC vs. Individual Ownership

Direct ownership exposes your personal assets to the full weight of U.S. legal claims. If a slip and fall accident occurs on the property, your global wealth could be at risk. An LLC limits this exposure to the assets held within the company. From an estate planning perspective, an LLC is far superior. Transferring membership interests in an entity is often a cleaner process than the complex probate procedures required for a deed transfer when an individual owner passes away. The Operating Agreement acts as your internal constitution, defining management roles and succession plans without the need for constant contract amendments.

FIRPTA and Tax Withholding Strategies

The Foreign Investment in Real Property Tax Act (FIRPTA) is a central concern during the eventual liquidation of your asset. Standard FIRPTA withholding requirements dictate that 15% of the gross sales price must be withheld by the buyer and sent to the IRS. For sales of a primary residence, this may be reduced to 10% for deals between $300,001 and $1,000,000, or 0% for those under $300,000. To manage these obligations, you'll need an Individual Taxpayer Identification Number (ITIN). If you have questions about how your entity structure impacts your final return, you can contact a professional advisor to review your specific tax posture.

Navigating the Real Estate Closing Process from Abroad

The trajectory from an executed purchase agreement to the final transfer of title is a choreographed sequence of legal and financial milestones. For the international investor, understanding US real estate contracts for foreigners requires a mastery of the closing phase, where the abstract terms of the contract transform into tangible ownership. This period, typically spanning 30 to 60 days, involves a rigorous verification of title, the finalization of insurance, and the preparation of the Closing Disclosure (CD). The CD is a mandatory document provided at least three days before closing that outlines every final cost, ensuring there are no financial surprises at the finish line.

A final walk-through is your last opportunity to verify the property's condition before the capital is released. Since physical presence isn't always feasible, many non-residents utilize trusted proxies or high-definition video walkthroughs to confirm that all agreed-upon repairs were completed. Discrepancies discovered during this stage, or a seller's failure to deliver the property in the promised condition, can create friction. If these issues aren't resolved through escrow holdbacks, they can escalate into international litigation, especially when the parties are operating under different legal systems.

Remote Signings and Notarization

Modern investment doesn't require a physical presence in a U.S. law office. Remote Online Notarization (RON) has become the standard in many states, allowing you to sign documents via secure video platforms. However, some jurisdictions still require physical "wet ink" signatures for specific deeds. In these cases, documents must often be notarized at a U.S. embassy or processed with a Hague Convention Apostille to be recognized as legally valid in the United States. Coordinating these logistics early is vital to avoid missing the strict "Time is of the Essence" deadlines discussed in previous sections.

Funds Transfer and Anti-Money Laundering (AML)

The movement of large capital sums into the U.S. triggers significant regulatory oversight under the Bank Secrecy Act. Title companies and lenders are required to perform "Know Your Customer" (KYC) checks and verify the source of funds to comply with FinCEN regulations. You must be prepared to provide a clear paper trail of your capital's origin, often dating back several months. As of March 1, 2026, new reporting requirements for non-financed residential transfers to entities mean that transparency is no longer optional. To ensure your transaction meets every regulatory hurdle without delay, you can schedule a professional real estate closing review.

The Intersection of Real Estate and US Immigration Law

Property acquisition is frequently the inaugural step in a sophisticated cross-border migration strategy. While it's a common misconception that purchasing a home grants residency, the reality is more nuanced. For the strategic investor, understanding US real estate contracts for foreigners involves recognizing how these assets can be leveraged within the framework of U.S. immigration law. A residential deed alone won't secure your status, but a commercial property contract structured as an active business enterprise can serve as the catalyst for your legal presence in the country.

For those pursuing an E-2 Visa, the investment must be substantial and, more importantly, active. This means the capital must be placed "at risk" in a commercial enterprise that has the capacity to generate more than a marginal living. Passive residential investments are excluded from this category. However, if your contract involves a multi-unit complex or a commercial facility used for operations, it may satisfy the requirements for a treaty investor application. Similarly, high-growth real estate ventures can bolster the portfolio of an O-1 Visa for entrepreneurs applicant by demonstrating significant commercial success and extraordinary ability.

The transition from property owner to Green Card holder is a long-term vision that requires precise legal engineering from the very first signature. Passive investment in residential property doesn't qualify for these paths, yet integrating your holdings into a larger corporate architecture can bridge the gap. It's about ensuring your real estate closing isn't just an end point, but a strategic entry into the American market. By understanding US real estate contracts for foreigners as a component of your broader immigration goals, you transform a static asset into a dynamic tool for residency.

Real Estate for E-2 Treaty Investors

To qualify for E-2 status, the funds used in the transaction must be irrevocably committed to the business. This "at-risk" requirement means that the contract should ideally be structured so that the capital is spent or legally bound before the visa is granted. Personal residences don't count toward this investment, but commercial spaces that house your business operations certainly do. Every clause in your purchase agreement should be reviewed to ensure it supports the narrative of an active, job-creating investment.

Legal Consultation and Strategic Planning

A real estate agent is an expert in market trends, but they aren't equipped to handle the complexities of cross-border tax or immigration law. Relying solely on a broker to draft your purchase agreement can lead to structural flaws that jeopardize your visa eligibility. A unified strategy ensures that your real estate, corporate, and immigration goals are in perfect harmony. To ensure your investment supports your future in the U.S., you should schedule a comprehensive real estate and immigration consultation.

Architecting Your American Investment Legacy

The transition from an initial offer to a secured title involves a complex web of legal safeguards, ranging from the precision of specific contingencies to the protective layer of corporate incorporation. Mastering the art of understanding US real estate contracts for foreigners ensures that your capital remains shielded while your long-term residency goals stay within reach. Whether you're navigating the latest transparency mandates or aligning a commercial purchase with an E-2 visa application, the structural integrity of your agreement is the most critical variable in your investment success.

Thriving in the American market requires a partner who understands the friction of international transactions and the nuances of cross-border law. With decades of experience in US-Italy legal matters, our team provides the bilingual support and specialized expertise needed for seamless LLC incorporation and real estate closings. Secure your US investment with a cross-border legal strategy—Contact Tosolini, Toniutti & Partners. Your vision for a U.S. portfolio deserves a foundation built on professional excellence and strategic foresight.

Frequently Asked Questions

Can a foreigner buy real estate in the US without a visa?

Foreign nationals can purchase U.S. real estate regardless of their current visa status. There are no federal restrictions on foreign ownership, though roughly 36 states enacted laws by late 2025 restricting purchases of agricultural land or property near military installations. It's vital to remember that ownership provides no automatic residency rights. You still need a valid visa to reside in the property.

Do I need an ITIN to sign a US real estate contract?

An ITIN isn't required to sign an initial purchase agreement, but you'll need one for the closing process and tax reporting. This number is essential for complying with FIRPTA withholding and reporting any future rental income to the IRS. It's best to start the application process early to avoid logistical delays in your final transaction timeline.

What is the FIRPTA withholding and how does it affect me?

FIRPTA is a mandatory 15% withholding tax on the gross sales price when a foreign person sells U.S. property. As of June 2026, the IRS allows a 0% rate for primary residences sold for $300,000 or less. A reduced 10% rate applies to primary residences sold for a price between $300,001 and $1,000,000. These funds are held to ensure capital gains taxes are paid.

Is it better to buy US property as an individual or through an LLC?

Holding property through an LLC is often superior because it limits your personal liability to the assets held within the entity. This structure prevents property related lawsuits from reaching your global wealth and simplifies the transfer of ownership for international families. It's a key component of a professional investment architecture that prioritizes asset protection and privacy.

What happens if I sign a contract but my visa is denied?

Unless your agreement contains a specific visa contingency, a denied visa doesn't automatically release you from your legal obligations. Understanding US real estate contracts for foreigners requires the inclusion of custom exit clauses that protect your earnest money if your immigration goals are not met. Without these protections, you risk a technical breach of contract and the loss of your deposit.

Can I use a foreign bank account to pay for my US property?

You can use a foreign account, but it often triggers extensive verification under the Bank Secrecy Act. Title companies require a clear "Source of Funds" paper trail to comply with anti-money laundering regulations. To avoid delays, many investors transfer their capital to a U.S. bank account several months before the closing date to ensure the funds are cleared.

Do US real estate contracts vary by state?

Contract forms and closing procedures vary significantly from state to state. In "attorney states" like New York, a lawyer must draft the agreement, while "escrow states" like California often use standardized title company forms. These regional differences impact everything from how you handle inspections to who manages the final exchange of funds and the recording of the deed.

How do I notarize US closing documents while I am in Europe?

You can utilize Remote Online Notarization (RON) or visit a U.S. embassy for physical notarization services. If your specific state requires "wet ink" signatures, the documents may also need a Hague Convention Apostille to be legally recognized in the United States. Coordinating these logistics early ensures you meet the strict deadlines mandated by your purchase agreement.

Comments