US-Italy Tax Treaty: A 2026 Strategic Guide to Cross-Border Compliance

- Gianni Mendes Toniutti, Esq.

- Apr 19

- 12 min read

What if the most significant threat to your transatlantic portfolio isn't market volatility, but a lack of structural alignment between two competing tax jurisdictions? For many high-net-worth individuals, the complexity of international law feels like an impenetrable labyrinth where a single misstep leads to double taxation. You likely understand that protecting your assets requires more than just intuition; it demands a precise blueprint that accounts for the intricate nuances of the us italy tax treaty. As we look toward the 2026 fiscal year, the necessity for a rigorous, engineering-focused approach to global compliance has never been more critical for those managing real estate or business interests in both nations.

We've designed this strategic guide to help you master the legal architecture of the us italy tax treaty, ensuring your cross-border investments remain protected from the scrutiny of the IRS and the Agenzia delle Entrate. It's about precision. You'll gain a clear framework for long-term tax planning that prioritizes both harmony and functional compliance. We'll examine the specific residency protocols, audit triggers, and profit protection strategies that will define the regulatory landscape over the next 24 months.

Key Takeaways

Navigate the foundational framework of the 1999 Convention to ensure your cross-border operations remain resilient and compliant within the 2026 fiscal landscape.

Identify the critical legal distinctions between active business income and passive investment streams to optimize the structure of your international portfolio.

Utilize the strategic relief mechanisms within the us italy tax treaty to effectively mitigate the risks of double taxation on your global assets.

Synchronize your real estate acquisitions and business entity planning with specific treaty provisions to safeguard capital gains and long-term property rights.

Learn how to integrate rigorous tax compliance into your broader legal roadmap to protect your green card status and cross-border residency goals.

Table of Contents Understanding the Framework of the US-Italy Tax Treaty Key Provisions: How the Treaty Categorizes Income Strategic Mitigation of Double Taxation Tax Strategy for Real Estate and Business Entities Integrating Tax Strategy into Your Cross-Border Legal Plan

Understanding the Framework of the US-Italy Tax Treaty

The us italy tax treaty represents a sophisticated bilateral framework designed to eliminate the friction of double taxation while deterring fiscal evasion between these two nations. Rooted in the 1999 Convention, this legal architecture remains the definitive blueprint for cross-border compliance as we enter 2026. By establishing Understanding the Framework of the US-Italy Tax Treaty, both governments provide a stable environment for the seamless flow of capital and talent. The treaty’s primary objectives focus on clarifying taxing rights and incentivizing international investment through predictable fiscal rules. For Italian nationals, these provisions serve as the essential starting point for any LLC incorporation. Without this foundation, the structural integrity of a transatlantic business would be compromised by conflicting tax claims and redundant liabilities.

The Purpose of the Treaty in Modern Cross-Border Relations

The treaty functions as a vital bridge, reducing tax barriers that might otherwise stifle trade between the US and Italy. It ensures that foreign entities receive fair treatment by preventing discriminatory tax practices based on nationality or corporate origin. By clarifying jurisdiction, the treaty also provides a predictable mechanism for resolving international litigation. This legal certainty allows partners to focus on innovation and long term growth rather than bureaucratic hurdles. It’s a tool for harmony in an increasingly complex global economy.

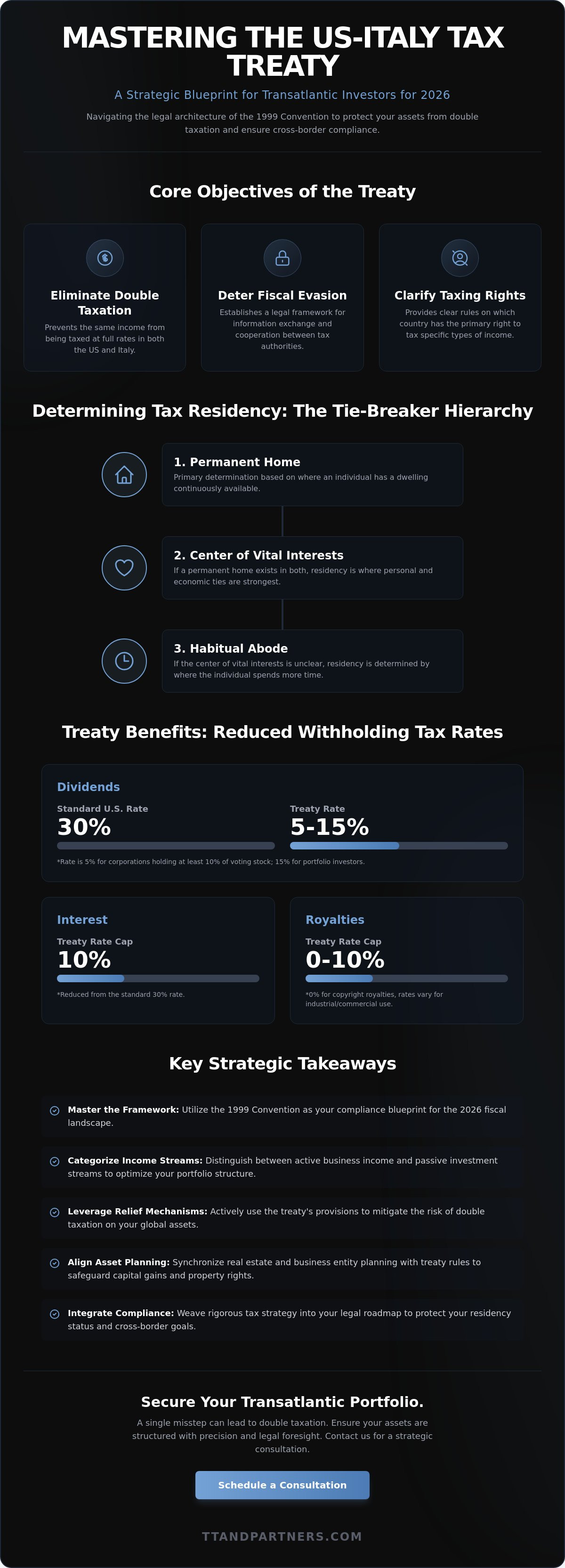

Determining Tax Residency: The Tie-Breaker Rules

Article 4 defines a "Resident" through a rigorous lens to ensure fiscal clarity for individuals and corporations alike. When an individual qualifies as a resident in both nations, the treaty applies a hierarchy of tie-breaker rules to determine a single tax home. This process prevents the same income from being taxed twice at the full rate in both jurisdictions.

Permanent Home: The primary location where an individual maintains a dwelling available for their use at all times.

Center of Vital Interests: The place where personal and economic ties, including family and professional relationships, are most concentrated.

Habitual Abode: The location where an individual spends the majority of their time during the calendar year.

In 2026, the habitual abode serves as a quantitative legal standard that measures the physical presence of a taxpayer over a 365 day cycle to resolve residency conflicts when other criteria remain ambiguous. If residency still isn't clear after these steps, the competent authorities of both states must settle the question by mutual agreement. This structured approach mirrors the precision required in architectural planning, ensuring every element of a taxpayer's status has a designated place within the legal fabric.

Key Provisions: How the Treaty Categorizes Income

The us italy tax treaty functions as a technical blueprint for fiscal residency and revenue categorization. It spans Articles 6 through 21 to define how specific income streams are treated across borders. The treaty distinguishes between active business income, which is generally taxed where the activity occurs, and passive investment income, which often receives preferential rates in the source country. The concept of "Beneficial Ownership" serves as the foundation for these benefits. It ensures that only the true recipient of the income, rather than a conduit or agent, accesses the reduced withholding rates. For a detailed legal framework, practitioners should consult the full text of the U.S.-Italy Tax Convention to understand the specific protocols signed in 1999 and ratified in 2009.

Taxation of Investment Income: Dividends, Interest, and Royalties

Article 10 establishes a tiered structure for dividends, significantly reducing the standard 30% U.S. withholding tax. Under these provisions, the rate typically drops to 15% for individual portfolio investors. For corporate entities holding at least 10% of the voting stock for a 12-month period, the rate can be as low as 5%. Article 11 and Article 12 address interest and royalties, often capping withholding at 10% or 0% for specific copyright or industrial equipment payments. These reductions provide Italian investors holding U.S. securities with a more efficient capital structure, preventing the erosion of returns through double taxation.

Business Profits and the Concept of Permanent Establishment

Article 5 defines the "Permanent Establishment" (PE), which is the threshold where a company's presence in a foreign country triggers local taxation. A fixed place of business, such as an office, factory, or workshop, constitutes a PE. Specific projects, like a construction site, only trigger PE status if they last longer than 12 months. For Italian companies, managing this physical and operational footprint is a matter of strategic precision. It's vital to coordinate these tax thresholds with the trade requirements of an E-1 visa, which requires a substantial and continuous flow of trade between the U.S. and Italy.

The interplay between these articles creates a balanced environment for international growth. Every structural decision, from where you sign contracts to how you repatriate profits, impacts your overall tax liability. If you're planning a complex cross-border expansion, reaching out for a strategic consultation can help ensure your business architecture remains both compliant and efficient in the 2026 fiscal landscape.

Strategic Mitigation of Double Taxation

Article 23 of the us italy tax treaty serves as the structural blueprint for preventing fiscal overlap. It ensures that income isn't taxed twice by assigning primary taxing rights to one nation while requiring the other to provide a credit or exemption. This creates a predictable framework for high-net-worth individuals and corporations. When disputes arise, the treaty functions as a critical instrument in international litigation, offering a clear hierarchy over conflicting domestic claims. Some practitioners worry that domestic legislation might override these protections. However, the "last-in-time" rule in US law means a treaty generally holds equal weight to federal statutes, maintaining its integrity unless specifically revoked by Congress.

The Foreign Tax Credit and Exemption Methods

The US employs the Foreign Tax Credit (FTC) to mitigate double taxation on Italian-sourced income. Under this system, taxes paid to the Agenzia delle Entrate are credited against US tax liabilities. In 2026, the complexity of the Section 904 limitation remains a hurdle, as credits are restricted to the US tax rate on that specific income category. Italy utilizes the "exemption with progression" method. While the foreign income itself isn't taxed in Italy, it's still factored into the calculation to determine the applicable tax rate for the individual’s remaining Italian income. This ensures the progressive nature of the tax system remains intact.

Navigating the Savings Clause and Its Legal Implications

The Savings Clause is a pivotal provision that allows the US to tax its citizens regardless of residency status. It maintains the status quo for the IRS, though specific carve-outs exist. Article 1, Paragraph 4 outlines these exceptions, protecting benefits for social security recipients, students, and teachers from being "saved" back into US taxation. The Savings Clause acts as a jurisdictional safeguard for the IRS to ensure that US citizenship remains the primary nexus for taxation regardless of treaty benefits.

Article 23: The primary mechanism for relief from double taxation.

Taxing Rights: Shared between nations to avoid overlapping claims.

Litigation Role: Resolves disputes through the Mutual Agreement Procedure (MAP).

Domestic Law: Treaty provisions generally prevail unless a specific override is enacted.

Maintaining compliance requires a deep understanding of these overlapping jurisdictions. The us italy tax treaty provides the necessary clarity to manage assets across borders without the burden of redundant taxation. Proper application of these rules protects the financial integrity of cross-border investments and ensures long-term stability.

Tax Strategy for Real Estate and Business Entities

Real estate serves as the anchor of a cross-border portfolio. Its physical permanence contrasts with the fluid nature of international tax law. Under the us italy tax treaty, Article 13 dictates that the right to tax gains from the sale of immovable property lies primarily with the state where the asset is located. For an Italian investor holding US property, this means the IRS maintains first-tier taxing rights. Success requires a meticulous alignment between legal title and tax reporting. Professionals must integrate these obligations directly into the architecture of a real estate closing to prevent structural leaks in the financial framework.

Impact on US LLCs and Italian Corporate Structures

The choice of entity acts as the foundation of the investment. US LLCs often utilize the "Check-the-Box" election, allowing them to be treated as disregarded entities for US purposes. However, the Italian Agenzia delle Entrate frequently classifies these same LLCs as opaque corporate bodies. This discrepancy creates a "hybrid entity" trap. If the entity isn't recognized consistently across borders, treaty benefits might vanish. Italian residents owning US LLCs must ensure their structure doesn't trigger double taxation on the same euro of profit. In 2026, the focus remains on ensuring the entity's characterization aligns with the beneficial owner's residency status.

Real Estate Transactions and FIRPTA Considerations

Selling US property triggers the Foreign Investment in Real Property Tax Act (FIRPTA). This law mandates a 15% withholding on the gross sales price, not just the gain. For many Italian sellers, this creates a liquidity vacuum. While the us italy tax treaty doesn't eliminate FIRPTA withholding, it provides the framework for claiming a refund or reduced rate through a withholding certificate, specifically Form 8288-B. Proper reporting involves filing Form 1040-NR or 1120-F to reconcile the actual tax due against the amount withheld. Strategic planning reduces the gap between the closing date and the eventual tax recovery.

Effective management of these assets requires a holistic view of the urban fabric and the legal codes that govern it. Each transaction is a design problem that requires both engineering precision and a vision for long-term sustainability. By coordinating tax planning with local closing protocols, investors protect the integrity of their international capital.

If you require a bespoke analysis of your cross-border holdings, contact our advisory team to discuss your specific requirements.

Integrating Tax Strategy into Your Cross-Border Legal Plan

The us italy tax treaty serves as the foundational framework for any trans-Atlantic engagement. It's the structural grid that determines where value is recognized and how assets are protected. Signing a contract without referencing this treaty is like starting a construction project without a site survey. You risk structural failure in the form of double taxation or regulatory scrutiny. In 2026, the complexity of global mobility demands a holistic approach. Legal counsel doesn't just review clauses; they design the environment where your tax strategy can thrive. This ensures every move you make aligns with your broader vision for a secure, dual-nation presence.

Why Legal Architecture Precedes Tax Filing

Tax compliance is reactive. It's the act of reporting what has already happened. Legal optimization is proactive. It's the design of the transaction itself. By structuring business operations through a lens of legal architecture, you minimize Permanent Establishment risks. Under Article 5 of the treaty, a fixed place of business can trigger massive tax liabilities if not managed carefully. Attorneys provide the necessary oversight, coordinating with cross-border tax preparers to ensure the legal substance matches the financial reporting. This partnership creates a resilient structure that withstands audits from both the IRS and the Agenzia delle Entrate. It's about building a system that functions with precision across two different legal landscapes.

Coordinating with International Litigation and Immigration Counsel

Your tax footprint directly impacts your legal standing. For those maintaining a green card, tax reporting isn't optional; it's a condition of residency. Claiming treaty benefits as a non-resident might offer short-term savings but could lead to the revocation of your immigration status. Every filing must be consistent with your visa or citizenship goals. The us italy tax treaty provides the specific legal mechanisms to resolve these conflicts before they reach a courtroom.

Treaty provisions also serve as a vital defense in cross-border litigation. They provide a clear set of rules to prevent arbitrary assessments by foreign tax authorities. Establishing a secure US-Italy legal presence requires this level of integrated thinking. It's about more than just numbers. It's about building a legacy that spans two continents with stability and grace. If you're ready to refine your international structure, contact our team for a strategic consultation.

Architecting Your Global Financial Future

Success in international investment requires more than just awareness; it demands a structured approach to the us italy tax treaty. As we move into 2026, the complexity of cross-border compliance necessitates a shift from reactive filing to proactive strategy. You've now seen how precise income categorization prevents redundant taxation and how specific real estate provisions protect your assets across two distinct legal systems. These guidelines aren't just bureaucratic rules; they're the building blocks of a sustainable international presence. Precision in these matters ensures your capital remains functional and your legacy stays secure.

Our team brings specialized expertise in US-Italy cross-border litigation and business architecture to ensure your investments remain resilient. We provide dual-jurisdiction legal support that bridges the gap between American and Italian regulatory environments. Don't leave your global portfolio to chance when you can build it on a foundation of professional certainty. Schedule a strategic consultation with our cross-border legal team to refine your 2026 plan. Your vision deserves a framework that's as ambitious as your goals. We're ready to help you navigate this landscape with confidence and clarity.

Frequently Asked Questions

Does the US-Italy tax treaty apply to US citizens living in Italy?

The us italy tax treaty applies to US citizens in Italy by providing essential mechanisms to prevent double taxation on the same income. While the US taxes based on citizenship, the treaty allows you to claim a Foreign Tax Credit to offset Italian taxes paid against your US liability. This legal structure ensures your global income isn't depleted by redundant fiscal demands from two different jurisdictions.

How does the treaty handle social security payments between the US and Italy?

Social security payments are governed by the 1978 Totalization Agreement rather than the primary income tax treaty. This separate pact ensures workers don't pay social security taxes to both nations on the same earnings. If an American company sends you to Italy for less than 5 years, you'll likely stay in the US system. It's a structured approach to preserving your long-term benefit eligibility across borders.

What is a Permanent Establishment and why does it matter for my business?

A Permanent Establishment is a fixed place of business, like an office or workshop, that triggers tax liability in the host country. Under Article 5 of the treaty, having this physical presence in Italy grants the Italian government the right to tax the profits generated by that specific location. It's the physical foundation upon which tax jurisdiction is built, requiring precise planning for any international business expansion.

Can the US-Italy tax treaty reduce my withholding on dividends?

The us italy tax treaty reduces the standard 30 percent US withholding tax on dividends to as low as 5 or 15 percent for eligible residents. To access these lower rates, you've got to meet specific ownership requirements and submit Form W-8BEN to the payer. This reduction facilitates a more efficient flow of capital, ensuring that your investment returns aren't eroded by excessive cross-border fiscal friction.

Do I still need to file a US tax return if I am covered by the treaty?

You're required to file a US tax return annually even if the treaty eliminates your total tax liability. The IRS requires disclosure of treaty-based positions on Form 8833 to maintain transparency and avoid penalties. Under Section 6114 of the Internal Revenue Code, failing to disclose these positions can result in a 1,000 dollar penalty for individuals. Compliance is the necessary documentation of your cross-border financial structure.

How does the "Savings Clause" affect Italian nationals with US Green Cards?

The Savings Clause in Article 1 allows the US to tax its residents and citizens as if the treaty didn't exist. Italian nationals holding US Green Cards remain subject to US global taxation on their worldwide income, despite their Italian ties. While specific exceptions exist for student or teacher income, this clause ensures the US retains its sovereign taxing rights over anyone it considers a domestic resident.

Does the treaty cover state-level taxes in the US?

The treaty doesn't cover state-level taxes in the US because it's a federal agreement between two sovereign nations. While your federal tax liability might be reduced, states like California or New Jersey don't always recognize international treaty provisions. You'll need to check the specific tax code of the state where you earned income. This distinction is vital for accurate financial modeling of your total US tax burden.

What happens if the US and Italy both claim I am a tax resident?

If both nations claim you as a resident, Article 4 provides tie-breaker rules based on your permanent home and center of vital interests. If you have a home in both countries, the treaty looks at where your personal and professional ties are most deeply rooted. These rules prevent the architectural collapse of your financial planning by providing a clear hierarchy for determining which nation has the primary right to tax.

Comments